The recent popularity of the Great Resignation idea , i.e. the expected wave of employee quits from their current jobs as the pandemia related economic conditions improve, has a lot to do with the growing optimism about the prospects of finally defeating the COVID-19 virus with vaccinations. The term itself was created by prof. Anthony Klotz (see 1 and 2). It explains the high probability of people quitting now by several factors among which are the no more need to cling to the job that was so crucial during the 2020 lockdowns and the growing demand for labor from most business sectors.

So what does the labor market data can tell us about the Great Resignation? I will try to explore several aspects of the jobs market development below using the US Bureau of Labor Statistics data. My calculations are just some back of the envelope quick estimates and deal with only one future scenario in order to simplify the math. The underlying basic future conditions are explained here

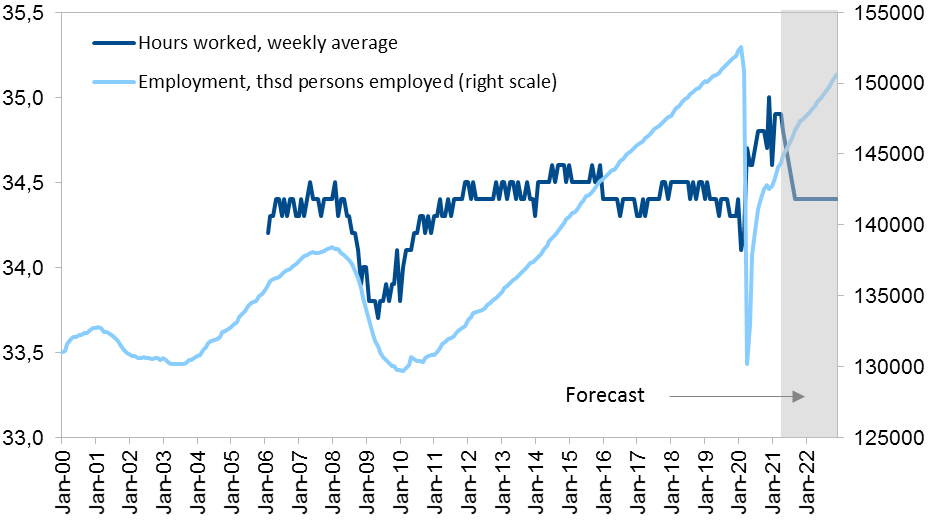

Employment and hours worked

The first chart shows the dynamics of employment and working hours starting from January 2000. Three observations are evident:

- in the two previous recessions businesses shed labor more gradually so it took about 3 years to reach the employment trough in 2000-03 and about 1.5 years in 2008-09 (ironically the latter seemed really harsh for me personally and for many other people who saw and experienced the then unprecedented layoffs avalanche);

- the 2020 slump in employment wasn’t accompanied by a reduction in hours worked as it was the case in 2008-09 – quite on the contrary, working hours significantly increased as employees were ready to stay in the office for longer trying to keep their jobs;

- in the previous two recessions it took 5-6 years for employment to recover to the pre-crisis levels.

With this in mind, the main assumptions about the future path of employment in the US can be described twofold. First, as the economic activity will most likely rebound much quicker the previous two recessions the employment will also recover at a faster pace. In the most probable scenario it will take 2.5 to 3 years from peak to trough and employment will return to the pre-COVID-19 level by end-2023 (2023 is not shown on the chart but it’s pretty clear where the trend line is directed). Second, as the labor market returns to balanced growth, working hours will go back to the 2010-20 average.

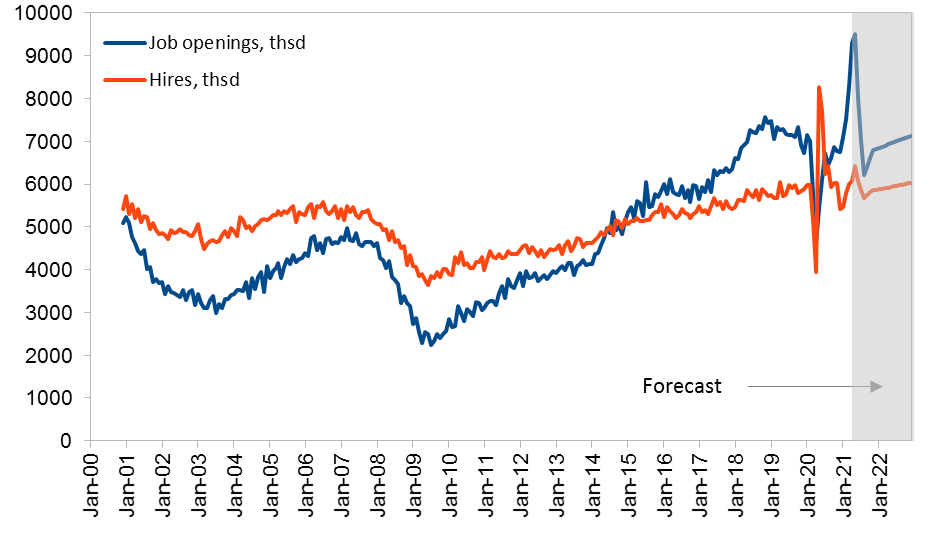

Job openings and hires

The major factor behind such spectacular (not spectacular enough someone may say) employment growth is the demand for labor that the majority of companies have nowadays. With most economies rapidly opening up after the severe lockdowns of the past 1.5 years businesses just need those workers back on-site in order to get on track with the production, revenue, and profit plans that suffered so much lately.

The feeling of just how coveted employees are can be seen in the recent jump in job openings. For January-April 2021 – the months the data is available – job opening have been soaring above 7 mln. per month which is an all-time record. At the same time, actual hires, which are highly correlated with job openings, also saw a pick up albeit not as a material one as in mid-2020.

The future path of the jobs market is not as outstanding as it is now. Nevertheless, in the basic scenario we can expect job openings to hover at a level of more than 7 mln. for about three more months. Subsequently the job creation rate – as measured by both job openings and hires – is most likely to subside by the end of 2021, after that returning to its long-term path.

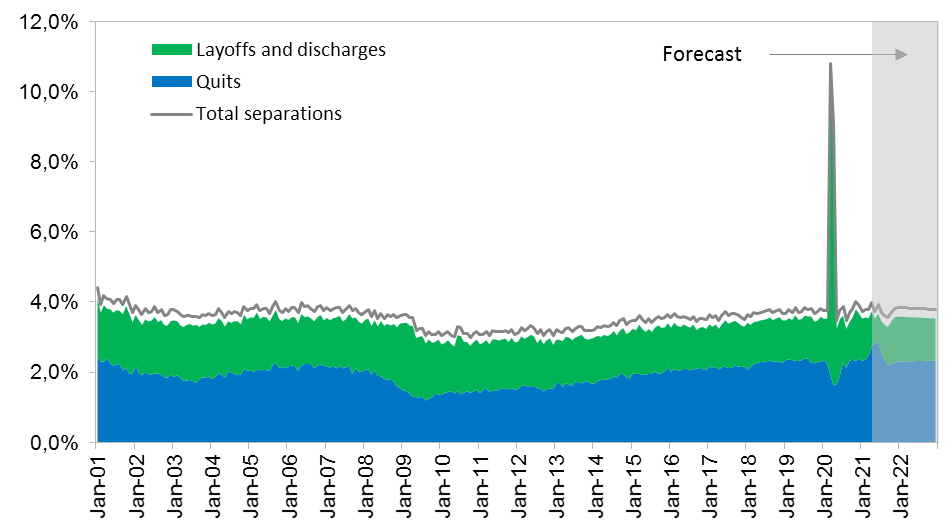

Layoffs and quits

Basically, the BLS data provides two major reasons for employees to leave their jobs: being laid off or quitting (there is a residual of other reasons but it’s small, stable, and does not substantially influence the calculations). The third chart shows the dynamics of the both as a percentage of the total employment. Several comments are applicable here:

- the 2020 peak in layoffs is indeed unprecedented but it was understandably short-lived and was mostly an uncertainty shock to all the corporate decision makers – see how later lockdowns did not engender such an erratic labor market reaction;

- as many observers rightly noted, the layoffs tsunami was accompanied by the sharp drop in employee quits because many people were just clinging to their jobs in the times of skyrocketing uncertainty about their future;

- since the start of 2021 the opposite dynamics can be seen with layoffs moving to their historically lowest levels and quits reaching their highest ever mark.

The Great Resignation wave

So what about the wave of resignations? As the third chart shows, we are currently going through this wave. However, it is highly likely that neither the wave will be as high as one can imagine, nor will it be as prolonged as many workers hope. Three crucial factors are the main reasons for this most probable future calming down scenario:

- in part the current quits wave is compensating the gap seen in 2020, and once this re-balancing is over most employees just will not risk their overall well-being in order to get a 10% raise or get rid of the slight dissatisfaction with their current boss;

- somewhat counter intuitively quits go hand in hand with job openings and hirings (but eventually it is all quite clear: the more job openings there are the more possibilities to find a better position and quit) so the Great Resignation wave will depend on job openings which will be fading off as discussed above;

- as soon as the employment figures are reaching their long-term trend levels the quits numbers will return to their own long-term slightly up-beat trend.

A few words about the labor market dynamics in the longer run. After the temporary volatile factors like compensating for the jobs lost due to the lockdowns are settled, the more fundamental labor market mechanics will come into play: productivity and wages being the major variables defining the future developments. Nevertheless, these questions to be answered adequately require a much more detailed and intricate analysis and math.

Overall, the Great Resignation wave is pretty real, and we are riding it at the moment. But it will not be as huge or as long-lasting as many people expect.